Acknowledgements

The author would like to thank Kelly Grieco, Bob Manning, Rachel M. Lee, Andrew Hyde, and Christopher Preble for comments on an earlier version of this paper. Standard caveats apply.

Introduction

There is an old Korean adage that “even rivers and mountains move over a decade.” This wisdom seems fitting for the landscape of international relations over the past 10 years. While much of the change initiated under Trump 1.0 starting with the 2017 National Security Strategy (NSS) signaled a clear break from the post-9/11 era, recent developments under Trump 2.0 suggest that US-led systemic change may be accelerating. South Korea has largely kept pace with these shifts even through the unexpected political turmoil in 2024-25; however, some of this change has already begun impacting the US-ROK alliance. This brief examines critical aspects of this transformation and considers Seoul’s options for the future of the bilateral relationship.

This paper argues that intensifying strategic competition between the United States and China is reshaping the regional and global security environment in ways that are placing growing pressure on the US–ROK alliance to adapt. This systemic change is affecting both the security and economic foundations of the bilateral relationship. In this context, the analysis highlights several developments likely to take shape in 2026 that will have consequences for the alliance: progress toward wartime operational control (OPCON) transfer, evolving force posture requirements in the Indo-Pacific, and the elevation of economic security and technology cooperation as core alliance functions. How effectively Seoul and Washington manage this transition will shape not only the future of the bilateral relationship, but also the alliance’s role in the broader regional order.

Alliance Modernization

One focal point in US-ROK relations gaining more attention recently is alliance modernization, which has been a topic of discussion for some time but has taken on a renewed urgency in Washington. Recent discussions increasingly frame modernization through the lens of U.S. demands for greater “strategic flexibility” and more balanced burden sharing. This framing is grounded in a broader emphasis on “peace through strength” and an approach described as “realism and restraint.”

As articulated in the latest National Defense Strategy (NDS), NSS, and the U.S. State Department’s Agency Strategic Plan, which have coincided with developments in Venezuela and Greenland, the Trump administration’s top priority appears to be securing the homeland and Western Hemisphere. While maintaining regional stability and a favorable balance of power in other parts of the world (e.g., Indo-Pacific) remain important objectives, the implicit assumption is that allies should shoulder a greater share of the burden for defense of their own backyard and play a more active role in the U.S. regional strategy.

The implications of this conceptualization of the U.S. national interest for the US-ROK alliance appear to be taking shape in several ways. At the 57th Security Consultative Meeting, Seoul committed to increase its defense spending to 3.5% of GDP and assume a leading role in the defense of the Korean Peninsula. An important dimension of this announcement was the agreement to certify the Full Operational Capability (FOC) of Future-Combined Forces Command (FCFC) Headquarters by the end of this year.

FOC is a key milestone in the Conditions-based Wartime Operational Control (OPCON) Transition Plan (COTP). It evaluates whether the FCFC meets Combined Mission Essential Task standards in command and control, intelligence and surveillance, firepower, and sustainment. The certification follows the Initial Operational Capability (IOC) assessment and precedes Full Mission Capability (FMC) verification, which is the final step that effectively authorizes OPCON transfer.

OPCON refers to the authority to command and direct military forces during wartime operations on the Korean Peninsula, a role currently exercised by a US-led Combined Forces Command (CFC). The CFC is commanded by a U.S. four-star general who also serves as the Commander of U.S. Forces Korea (USFK), and OPCON transfer would shift wartime command authority to a South Korean-led command while preserving the combined US–ROK military structure and the U.S. commitment to defend South Korea. The new administration in Seoul appears to welcome the latest development as an opportunity for South Korea to finally achieve a more autonomous national defense in the near future.

It is important, however, to not view OPCON transfer in isolation, but as part of a broader process of modernization — one that entails a restructuring of the Combined Forces Command (CFC) and the evolution of US-ROK force posture in response to shifting global and regional strategic demands. As stated in the latest NDS, “South Korea is capable of taking primary responsibility for deterring North Korea with… limited U.S. support… [and] this shift in the balance of responsibility is consistent with America’s interest in updating U.S. force posture on the Korean Peninsula.” In short, the latest developments signal a potential change in the security relationship in keeping with the broader context of changes underway in other parts of the world. The question is where South Korea stands on the broader regional strategic challenge in the Indo-Pacific.

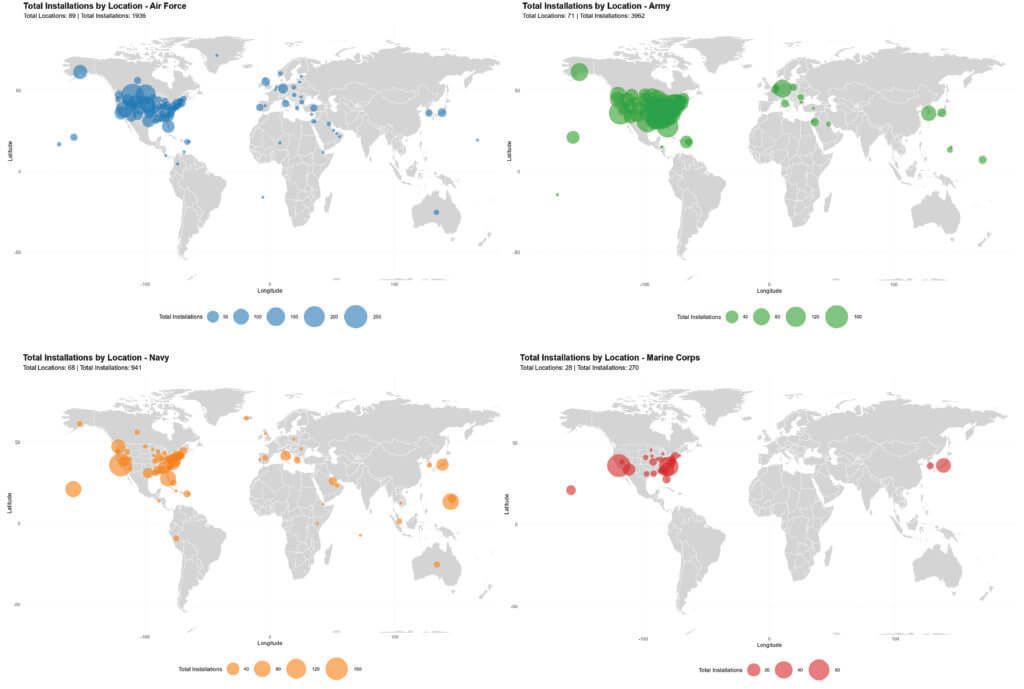

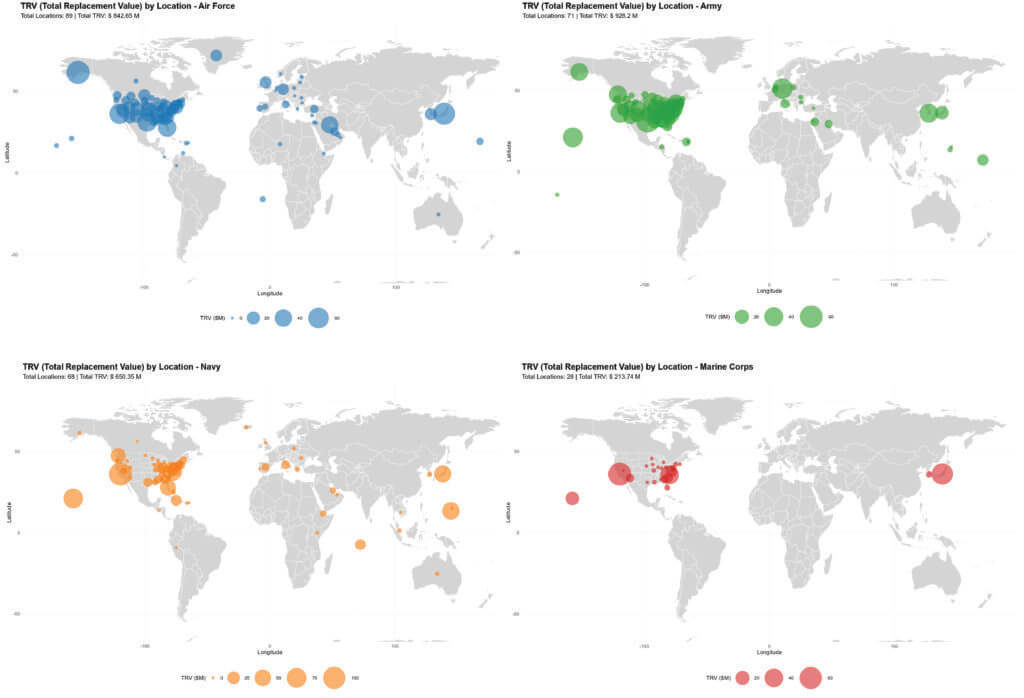

As of today, the U.S. force presence in South Korea is the second largest in the region after Japan. According to the latest U.S. Department of Defense Base Structure Report, the United States military maintains approximately 80 sites in South Korea, with a total replacement value exceeding $56 billion — reflecting a force posture still heavily oriented towards the U.S. Army (See Figures 1 and 2). By contrast, Japan hosts a total of 98 sites with a combined replacement value of nearly $193 billion, with basing infrastructure primarily supporting the U.S. Air Force, Navy, and Marine Corps operations.

Figure 1. U.S. Military Installations Around the World, 2025

Source: US DoD Base Structure Report

Figure 2. Total Value of U.S. Military Installations by Location, 2025

Source: US DoD Base Structure Report

This divergence underscores a long-standing perception about the division of labor within the alliance network in Northeast Asia: South Korea as a deterrence platform against North Korea, and Japan as a regional hub for air, naval, and expeditionary operations of U.S. forces. Commander of U.S. Forces Korea (USFK), General Xavier Brunson has pushed back against this idea by suggesting a conceptualization of South Korea as a central operational hub “inside the defensive perimeter.” Others have suggested that the deployed capability on the peninsula should be rebalanced to address the strategic challenge of being able to handle non-peninsula contingencies. With or without OPCON, the forthcoming Force Posture Review could signal some significant adjustments to this configuration as the United States seeks what Admiral Aquilino described as “a widespread distributed force posture west of the international date line.”

In this context, South Korea should deliberate carefully over potential changes to the institutional foundations of the alliance. Decisions surrounding command, basing, and force posture will shape not only South Korea’s national defense but also whether the US-ROK alliance evolves from a peninsula-focused deterrent into a broader strategic node within the U.S. regional security architecture. As some have suggested, reconfiguring basing of USFK to incorporate more air and land-based missile capabilities can be a part of this effort. Another possibility is to consider naval basing to take advantage of South Korea’s shipbuilding capacity. In all of these options, interoperability will be an important consideration. The choice is South Korea’s to make provided its complementarity with the U.S. regional strategy.

The 70-year-old alliance has worked well for both the United States and South Korea, as there has not been a second Korean War since the signing of the Armistice and the Mutual Defense Treaty in 1953. In exchange for U.S. security guarantees, South Korea has repeatedly demonstrated its commitment as a dependable ally, deploying troops to Vietnam, Iraq, and Afghanistan, and continuing to support efforts on peacekeeping and maritime security.

Over time, the bilateral relationship has evolved beyond a narrowly defined military alliance. It now encompasses cooperation across technology, industrial policy, and economic security domains, where leading South Korean firms play an increasingly visible role to support U.S. industrial revitalization and supply-chain resilience. This evolution reflects a broader transformation of the alliance — from one centered on the military to one increasingly oriented towards shared responsibility in the economic arena to which we now turn our attention.

Economic Security and Technology Cooperation

The two rounds of summits in 2025 between Presidents Lee Jae Myung and Donald Trump resulted in the announcement of a Joint Fact Sheet in November 2025 outlining South Korea’s pledge of $350 billion in additional investment into the United States, including $150 billion in shipbuilding. Seoul also agreed to spend $25 billion on U.S. military equipment purchases by 2030 and to contribute an additional $33 billion to the cost of USFK. In return, South Korea secured a reduction in U.S. tariffs on Korean goods from 25% to 15%, as well as U.S. support for “the process that will lead to the ROK’s civil uranium enrichment and spent fuel reprocessing.”

While there were other notable elements — including discussion of the potential for South Korea to build nuclear-powered attack submarines — the core economic dimension of the summits consisted of a series of Memoranda of Understanding (MOUs) announced between Korean and U.S. firms across sectors ranging from aviation and shipbuilding to nuclear power, critical minerals, semiconductors, and LNG. A separate government-to-government MOU reaffirmed cooperation in AI adoption and innovation, advanced radio access networks (RAN) and 6G, pharmaceutical and biotechnology supply chains, quantum computing, space, and talent exchange.

Although critics question whether these MOUs will generate binding commitments or commercially viable outcomes, the Joint Fact Sheet and summits all signal that South Korea remains interested in the United States’ broader industrial revitalization effort. There are several reasons for this. First, other U.S. allies in Europe and Japan faced similar pressures yet chose restraint over retaliation, underscoring a broader pattern of alliance discipline. This dynamic is especially salient for South Korea as a treaty-bound ally for whom the relationship with the United States remains foundational to its national security interests.

Second, both the South Korean government and major chaebol conglomerates view relations with the United States as a long-term strategic proposition that extends beyond Trump 2.0. Change can be disruptive, but it can also be an opportunity. While U.S. policy after 2028 remains uncertain, American leadership in emerging technologies and the global dominance of the dollar are unlikely to change in the near term.

Finally, the two economies are so deeply intertwined that unwinding these linkages would be costly for both sides. From a macroeconomic perspective, the U.S. is South Korea’s second-largest trade partner, and trade plays an outsized role in the Korean economy, accounting for over 80% of its GDP. South Korean corporate investment in the United States also allows its subsidiaries to cushion policies that can negatively impact Korea’s export performance — though this calculus could look different if the underlying conditions also change.

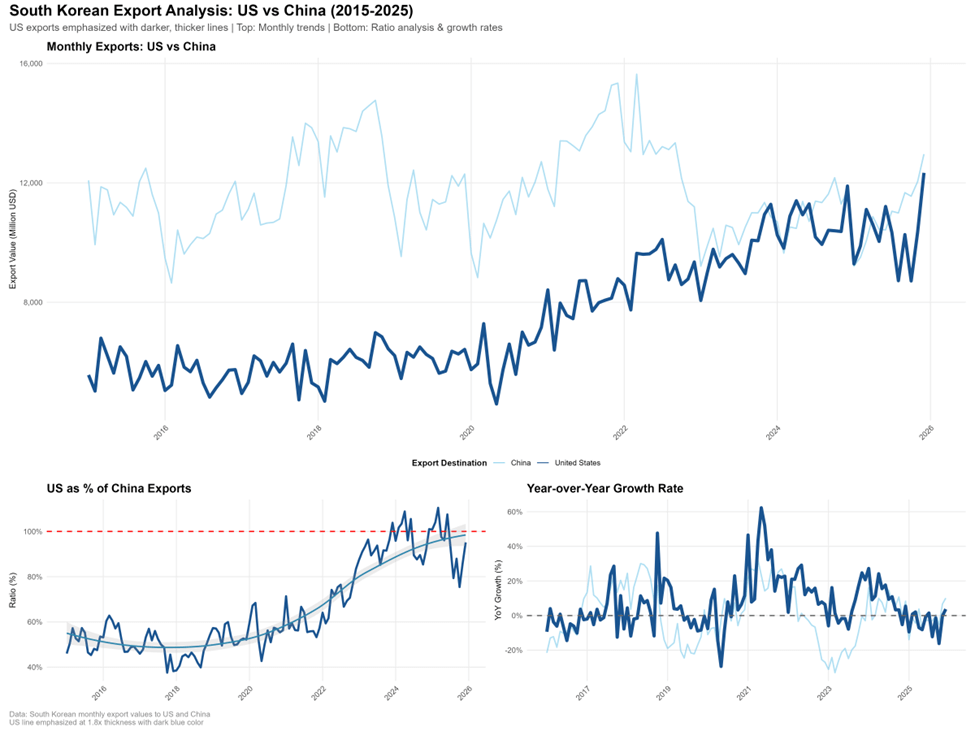

Figure 3. Monthly South Korea Export of Goods to the U.S. and China, 2015-2025

Source: Korea Customs Service

It is still too early to determine whether U.S. tariffs have had a significant impact on South Korea’s overall trade performance even though trade with the U.S. fared comparatively worse than that with other regions in 2025. In 2025, for instance, South Korea’s export of goods to the United States totaled $122.86 billion, which was a 3.8% decline from 2024 ($127.76 billion). In comparison, South Korea’s export to mainland China only declined by 1.67% from $133 billion in 2024 to $130.78 billion in 2025. Comparison of monthly figures for exports to the U.S. and China show a competitive landscape (See Figure 3).

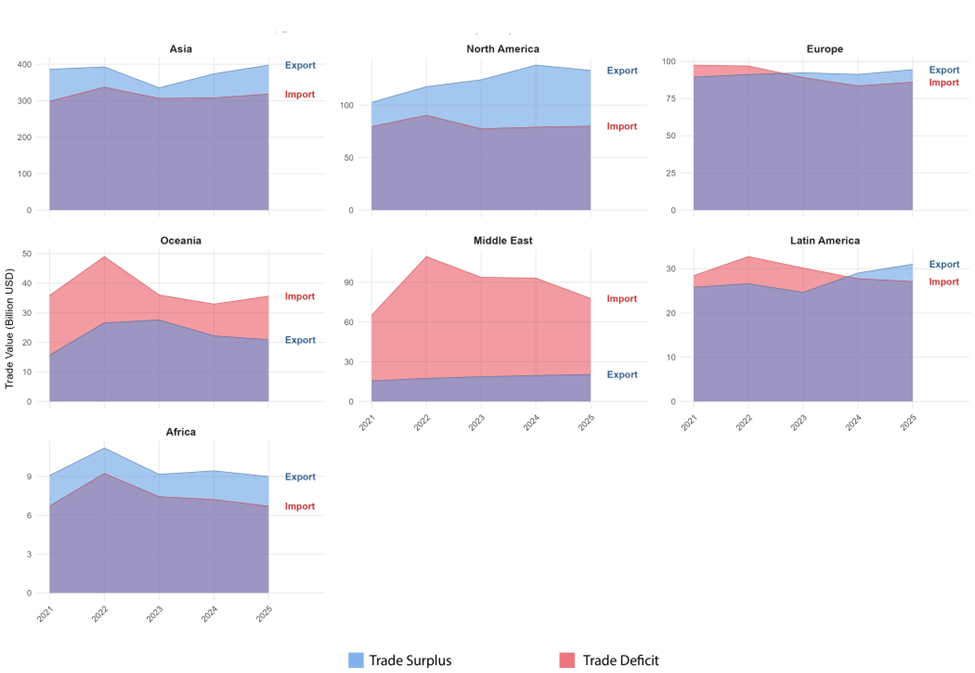

While South Korea’s overall trade in goods increased across regions like Asia ($681.5 billion à $716 billion, +5%), Europe ($174.8 billion à $180.5 billion, +3.29%), Latin America ($56.7 billion à $58.1 billion, +2.3%), and Oceania ($55.1 billion à $56.5 billion, +2.5%) during the same period, total trade in goods with the United States contracted by 1.8% from nearly $200 billion in 2024 to $196 billion in 2025 (See Figure 4).

Figure 4. Annual South Korean Trade of Goods by Region, 2021-2025 (Unit: in Billion $)

Note: This layered representation shows red area on top representing the amount that import exceeds export (trade deficit), and light blue area representing the amount that export exceeds import (trade surplus). Source: Korea Customs Service

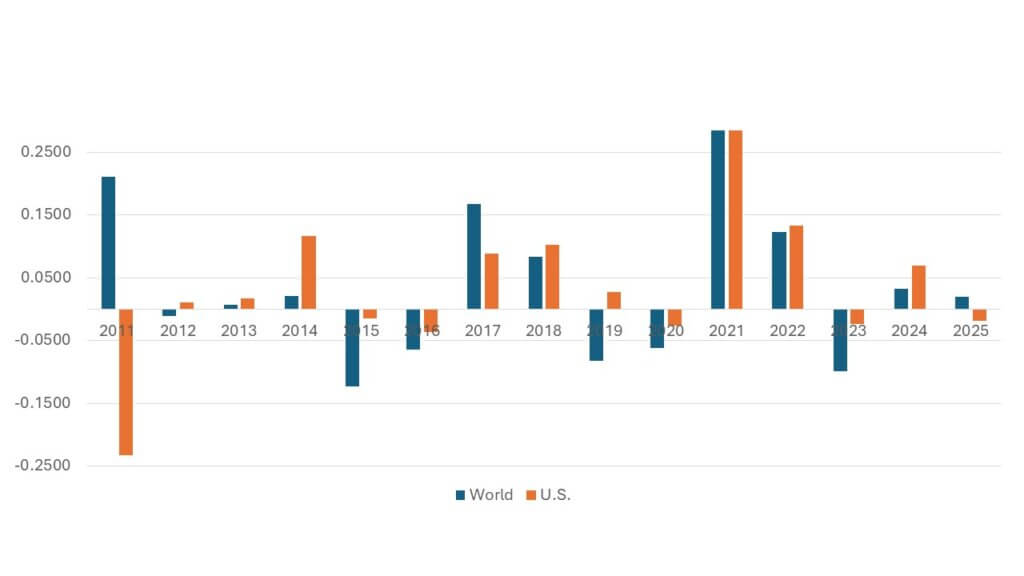

In fact, this is the first year since 2011 when South Korea’s trade in goods with the U.S. contracted while its global trade grew in the same year (See Figure 5).

Figure 5. Annual Change in South Korean Trade, 2011-2025 (Unit: %)

Source: Korea Customs Service

If the Trump administration’s objective is to revitalize domestic industrial capacity and promote growth through more vibrant and fair commercial exchange with allies like South Korea, the latest data offer limited grounds for optimism. One way to address this gap is to deepen areas of collaboration that build on the outcomes of the recent summits and the groundwork laid by the previous administration. In particular, the 12 strategic technologies identified by the South Korean government overlap substantially with U.S. Critical and Emerging Technologies (See Table 1).

Table 1. South Korean Strategic Technologies and U.S. Critical and Emerging Technologies

[table “” not found /]Source: Ministry of Science and Information Communications Technology and Executive Office of the President of the United States

While the Biden administration utilized the Critical and Emergency Technology (CET) Dialogue as a consultative tool to coordinate in a subset of these sectors among the two countries, the alliance still lacks a comprehensive framework that moves beyond consultation toward joint implementation. Early signs of increased investment activity across several strategic sectors suggest both momentum and opportunity. Establishing a standing coordinating body — co-chaired at the deputy ministerial or undersecretary level — with authority over supply-chain resilience, export controls, standards-setting, and industrial policy coordination would help to institutionalize this momentum. Such a mechanism could serve as the foundation for joint R&D projects, establishing joint investment vehicles, identifying trusted supplier networks, and developing dual-use technology pipelines, anchoring economic security as a core pillar of the alliance.

Conclusion

The US–ROK alliance has entered a period of systemic change driven by shifting U.S. priorities and intensifying strategic competition, altering both the costs and benefits of the bilateral relationship. The question facing Seoul and Washington is no longer whether the alliance should change, but whether it will do so in a deliberate and coordinated manner.

With respect to security, alliance modernization through OPCON transition, evolving command arrangements, and potential adjustments to force posture reflect a broader expectation that South Korea assume greater responsibility for the defense of the peninsula and a more active role within the U.S. regional strategy. Managed well, these changes can strengthen deterrence and enhance South Korea’s strategic autonomy without weakening the credibility of U.S. commitments. Managed poorly, they risk creating ambiguity over roles, missions, and decision-making authority at a time of heightened regional uncertainty.

In parallel, economic security and technology cooperation have emerged as indispensable pillars of the alliance. The 2025 summits and Joint Fact Sheet underscored the degree to which South Korea is already embedded in U.S. industrial revitalization and supply-chain resilience efforts. Yet the limits of ad hoc coordination and non-binding MOUs are increasingly evident. Without institutional mechanisms that translate alignment into implementation, economic cooperation will remain vulnerable to political cycles, shifting trade pressures, and divergent regulatory approaches.

Taken together, these trends point toward a necessary next phase in the evolution of the US-ROK alliance. This does not imply decoupling or strategic overreach. Rather, it reflects the reality that an alliance designed for a different era must now operate across multiple domains — military, economic, and technological — where credibility rests on shared decision-making and sustained coordination.

For South Korea, the challenge is to shape this transition proactively, ensuring that greater responsibility is matched by greater voice and institutionalized influence within the alliance. For the United States, the task is to recognize that alliance durability in an era of systemic change depends less on extracting concessions than on building frameworks that enable trusted allies to act as partners. Whether the US–ROK alliance can meet this test will determine not only its relevance on the Korean Peninsula, but its role in the evolving regional order.

Current Geopolitics Shift Deep-Sea Mining Debates