")

Most observers predicted the recent Supreme Court (SCOTUS) ruling striking down President Trump’s International Emergency Economic Powers Act (IEEPA) tariffs; however, the decision raises new doubts and questions about trade with the United States for exporters from countries like South Korea. This explainer discusses what the recent ruling means for trade between South Korea and the United States and how South Korea may respond to relations with the U.S. in the coming days.

What Next?

During an interview in January, U.S. Trade Representative Jamieson Greer stated that the administration would utilize other measures to reimpose a new set of tariff measures if the Supreme Court ended up ruling against the administration. The White House announced immediately thereafter that the administration would make use of Section 122 of the Trade Act of 1974 to impose a 10% global tariff for 150 days after which Congress has the right to allow the president to extend this tariff or not. The next day, President Trump declared that this rate would increase to 15%. Meanwhile, several Republican members of Congress have broken ranks to oppose the president’s use of tariffs while experts have pointed out that the tariff authority under Section 122 does not legally apply in this case because there is no balance of payments problem.

However, there is more dry powder in the administration’s keg even if Section 122 is unavailable for the administration. Section 338 of the Tariff Act of 1930 grants the administration a broad authority to impose tariffs if other countries “uniquely discriminate” against the United States. Section 232 of the Trade Expansion Act of 1962 and Section 301 of the Trade Act of 1974 are also measures that the administration has at its disposal, but they require an investigative review, which means the administration would need time to reimpose new tariffs if it were to invoke these measures. There is also the issue of the refund of over $175 billion under the IEEPA tariffs, with a backlog of over 3,000 lawsuits that will now be litigated in the lower courts. Regardless of the subsequent response by the administration and Congress, the world will have to hold its breath and see which new measures will be used to reimpose a new set of tariffs and how that might impact the trade landscape, if at all. But what does this new ruling mean for countries like South Korea?

It was clear long before this Supreme Court ruling that trade with the United States was becoming increasingly precarious for South Korea. In the latest round of the trade saga between South Korea and the United States, President Trump’s Truth Social posting and comments raised new doubts about the meaning of the November agreement between the two countries, which effectively lowered South Korea’s IEEPA tariff from 25% to 15%. This is not the first time that the two countries have had trouble putting this issue to bed.

The earliest announcement of a potential deal between the Trump and Lee administrations can be traced back to as early as July 2025, timed with President Lee Jae Myung’s visit to Washington for his first summit with President Trump. That deal was never formally announced until the second meeting between these two leaders on the sidelines of the Asia Pacific Economic Cooperation (APEC) Summit in late October.

A recent social media posting by President Trump suggested that South Korea is purposefully delaying the first tranche of investment worth $20 billion for this year. Seoul responded with a series of high-ranking official visits to Washington at around the time that the USTR issued an announcement that it is reviewing the possibility of raising the tariff level back up to 25%. President Trump’s last statement on this matter suggests, however, that he will not be following through with his most recent threat… or will he?

With the announcement of the new Supreme Cout ruling, can we even question the existence of any “deal” between the U.S. and South Korea when the agreement was that the latter would receive a reprieve on the now-unconstitutional IEEPA tariff (a reduction from 25% to 15%) in exchange for $350 billion investment in the United States? One argument may be that South Korea has the option to delay the implementation of its investment. However, the Trump administration could recreate the threat of a 25% tariff under Section 301 authorities, and still has sectoral tariffs through the Section 232 tariffs on auto and steel that it can threaten to ratchet up, or it could impose additional tariffs on pharmaceutical imports or semiconductors, which are tied to the terms of the November agreement. This likely explains why the South Korean Ministry of Industry, Trade, and Resources (MOTIR) decided to maintain the terms of the November agreement.

Even with the existing deal in place, Seoul should keep in mind that one important dimension of the SCOTUS decision is the statement that the Court “would not expect Congress to relinquish its tariff power through vague language, nor without careful limits,” meaning that there would have to be an explicit delegation of this power to the executive branch. Article I, Section 8 of the U.S. Constitution is clear in no uncertain terms that Congress has the power “to regulate Commerce with foreign Nations.” This acknowledgement by the Court suggests that there is likely to be more legal challenges on future tariff measures that the Trump administration pursues unilaterally. If so, as long as the domestic disputes on tariffs continue, businesses will face an uncertain environment that will affect their trade and investment.

Putting aside tariffs, an important future development to watch for is the Trump-Xi summit in April, which introduces yet another layer of complexity. Will there be a new deal between the U.S. and China, and if so, how long will that last? And will there be extreme swings in policy during the winding and unwinding of regulatory restrictions on trade and investment with China?

The Impact on South Korea’s Trade Performance

The latest SCOTUS decision demonstrates that, tariff or no tariff, uncertainty will be a lasting feature of U.S. trade policy, and this will affect South Korea’s trade performance. To illustrate, we examine South Korea’s trade data, which shows that overall volatility in trade increased not only for the United States but also for other countries. South Korea’s adaptive response also signals an effort to have a more diversified trade portfolio, which may mean reduced dependence on any one or few large trade partners.

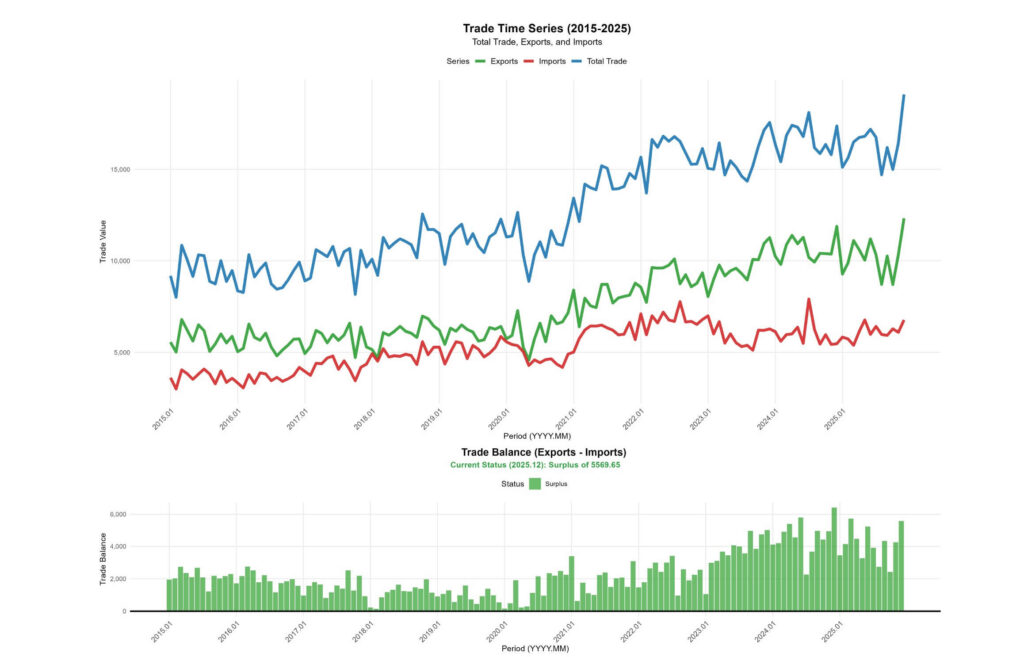

Figure 1. Monthly South Korean Trade with the U.S., 2015.01 – 2025.12 (in $ Million)

Source: Korea Customs Service

First, the annual data on overall trade in goods between the United States and South Korea shows a marginal decline of 1.8% from nearly $200 billion in 2024 to $196 billion in 2025, which was partly attributed to a decrease in the export of goods from South Korea to the U.S. from nearly $128 billion in 2024 to $122.86 billion in 2025. This is significant since the last decrease in the export of goods to the U.S. was in 2016 when it drew down by 4.8%. One reason for the more muted decrease this year was the increased demand for semiconductors and machinery as the U.S. works to ramp up its investment in AI infrastructure.

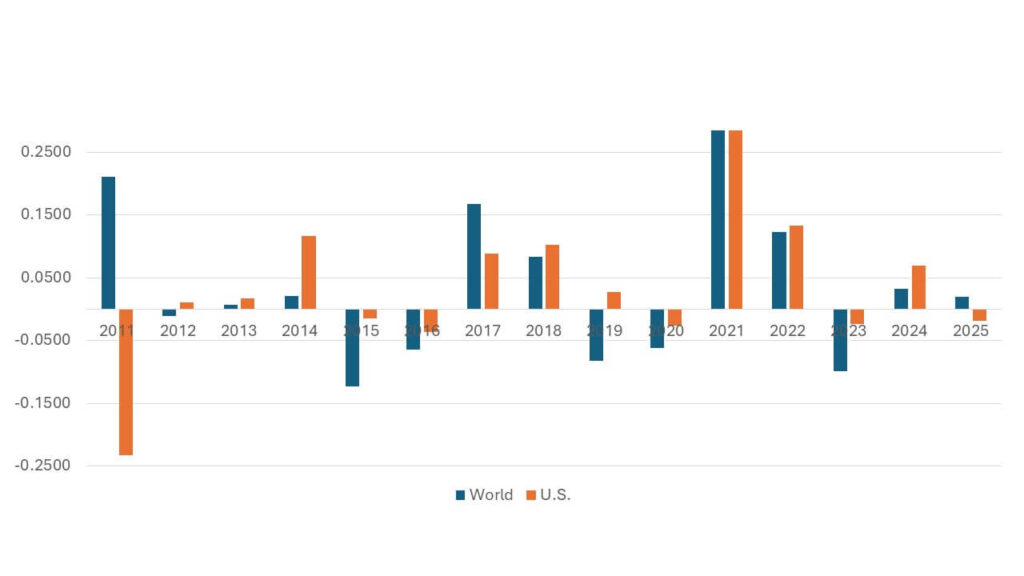

Figure 2. Annual Change in South Korean Trade, 2011-2025 (Unit: %)

Source: Korea Customs Service

The trade balance declined for the first time since 2019 from 55.6 billion in 2024 to 49.5 billion (-11.1%), which can be attributed to a combined effect of a decrease in exports and an increase in imports (+ 1.7% from $72.1 billion in 2024 to $73.35 billion in 2015) with the U.S. One may argue that the Trump administration’s trade policy had a sizable impact.

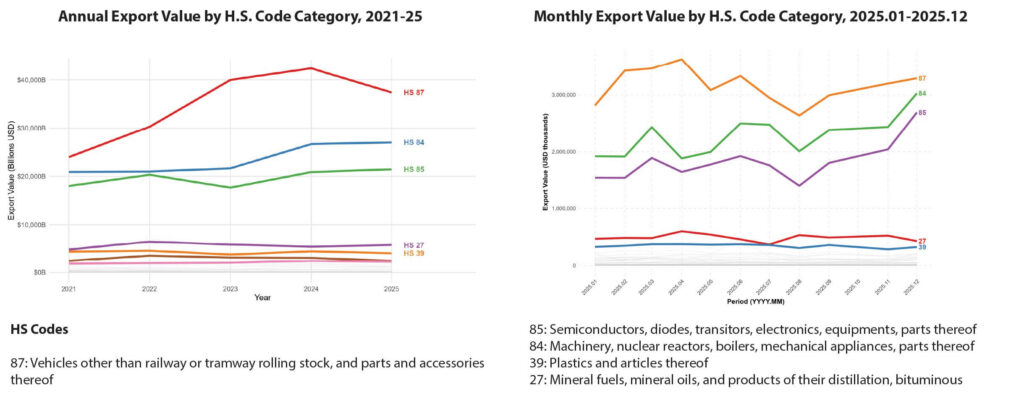

Figure 3. Korean Exports to the U.S. by HS Code Categories

Looking more closely at the monthly trade data by item category, we can see a significant decline in automotive related exports (HS 87) during Q2 and Q3 2025. Much of this decrease came after April with consistent monthly recovery after the summit in August. A similar pattern can be observed for two other major export categories but at a smaller scale – semiconductors (HS 85) and machinery (HS 84). In short, what we see is sectoral trade performance moving with the announcements related to tariffs, suggesting that what the administration does directly impacts sectoral trade performance.

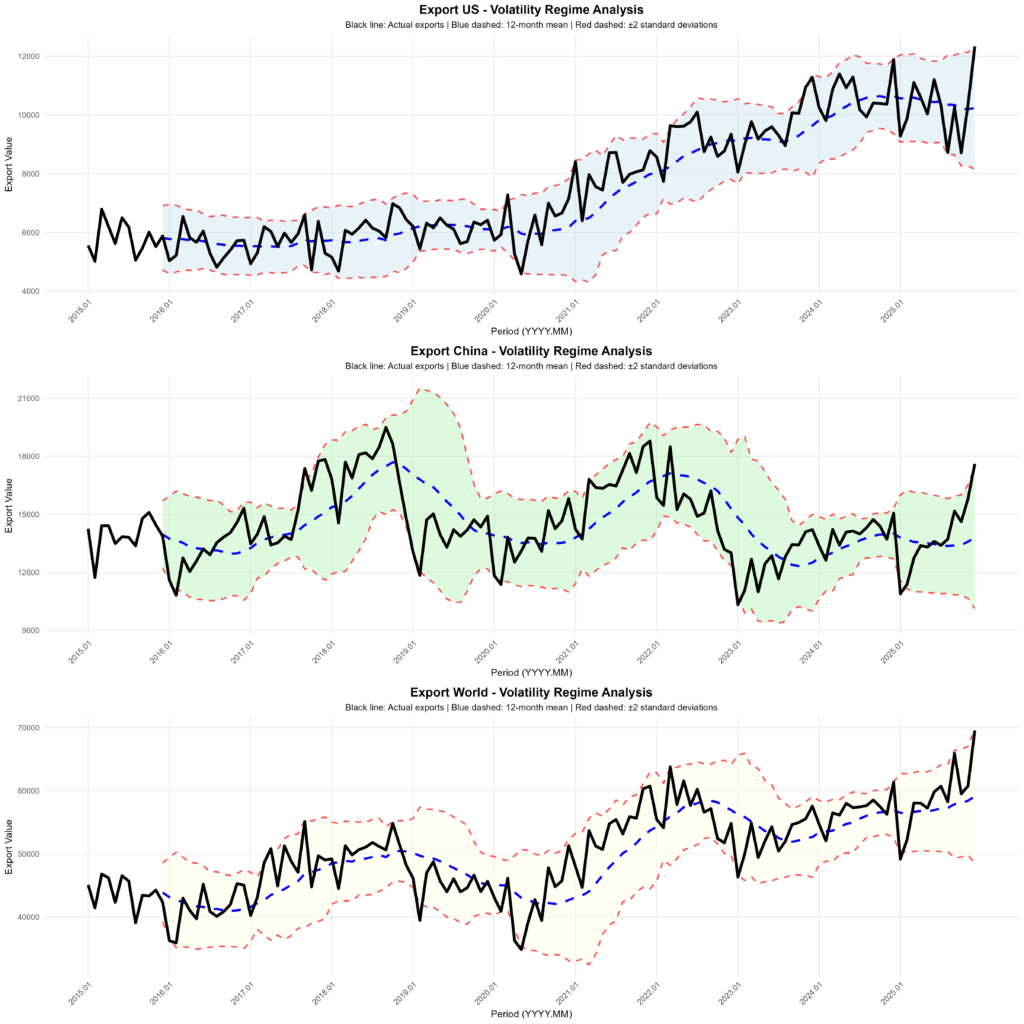

Figure 4. Volatility in Monthly Export to the U.S., China, and World, 2015.01 – 2025.12 (in $ Millions)

Note: The dashed line represents 12-month moving average, and the band represents +/- 2 standard deviation of the 12-month moving average of export values. Source: Korea Customs Service

With regard to trade volatility over time as measured by the twelve-month rolling standard deviation of South Korea’s trade with the U.S., China, and the world, we see an increase in overall volatility during 2025 in all three cases with the two-standard deviation band widening in 2025 compared to 2024. Another interesting pattern is that the data shows South Korea’s trade with China being more volatile than trade with the United States, which can be traced back to as early as 2017-18. That is, the two-standard deviation band of the twelve-month moving average is larger for China and the world when compared to that of the U.S. This implies that South Korea has made larger adjustments to its trade with China and the rest of the world due to changing U.S. policies.

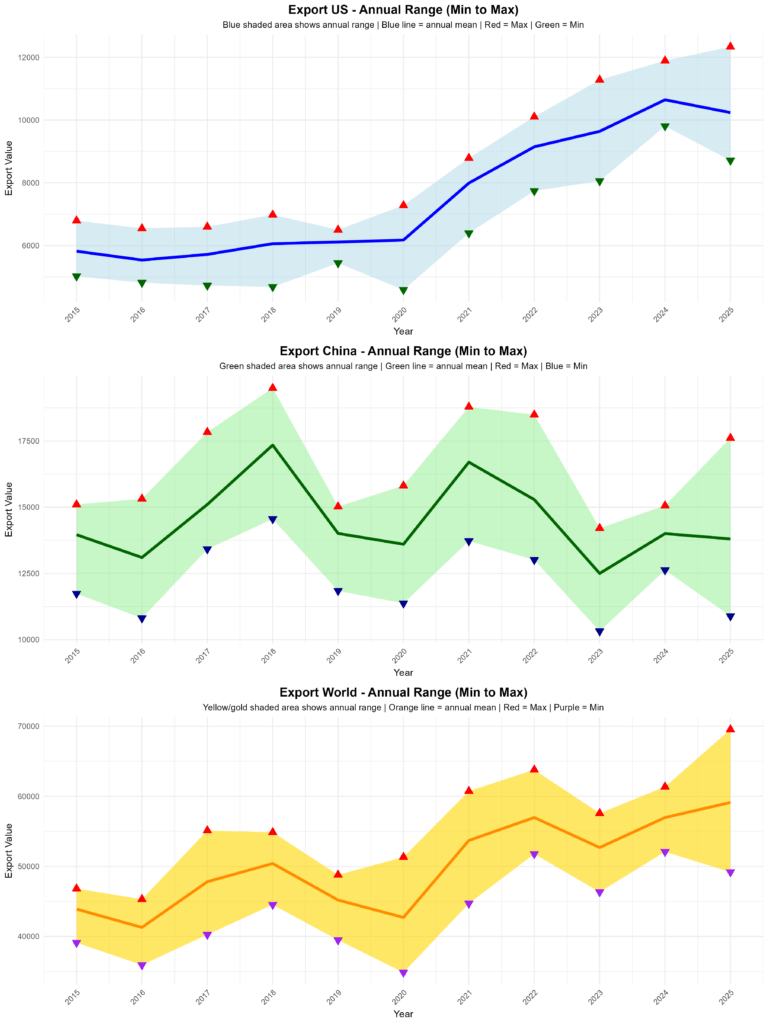

Figure 5. Annual Range for Exports to the U.S., China, and World, 2015.01 – 2025.12 (Unit: in $ Million)

Source: Korea Customs Service

Similar results can be found when comparing the annual range or difference between the monthly maximum and minimum in each year for South Korea’s exports to the U.S., China, and the world. What we see is a marked increase in 2025 compared to 2024. However, that increase in range was more pronounced for China than for the United States. For instance, the range for China in 2025 was $6.72 billion (Maximum: $17.61 billion in December; Minimum: $10.89 billion in January), which was an over 2.7-fold increase from $2.433 billion in 2024 (Maximum: $15.06 billion in December; $12.627 billion in February). For the U.S., the range was $2.08 billion in 2024 and $3.62 billion in 2025, which is only an approximately 1.7-fold increase.

What these findings show are: 1) trade volatility with the U.S. in 2025 was generally higher than in 2024; but 2) trade with China and other countries has been generally more volatile when compared to that of the United States. We can reason from this that changes in U.S. trade policy are having a significant impact on South Korea’s trade performance and volatility.

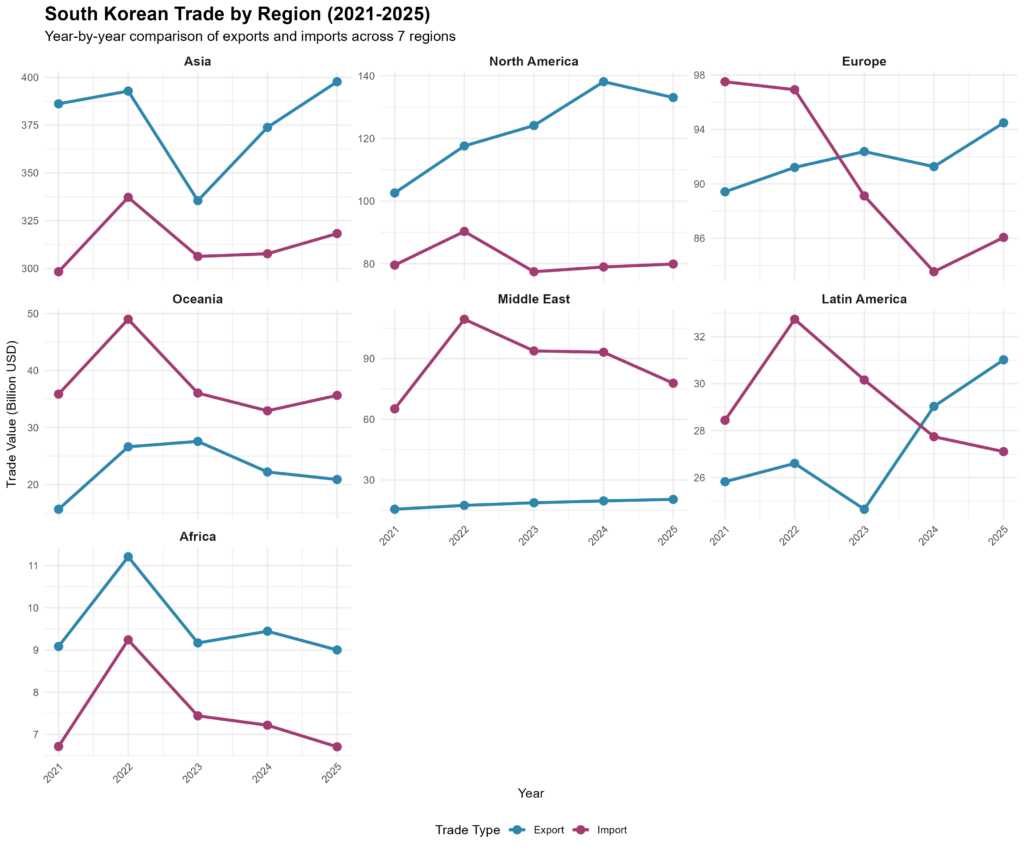

Figure 6. Annual South Korean Trade by Region, 2021-25 (in $ Billion)

Source: Korea Customs Service

According to the OECD, trade accounted for 85% of South Korea’s GDP in 2024. Looking ahead, the South Korean economy’s dependence on global trade will continue given the country’s declining population and relatively small domestic market. What this means is that if the U.S. continues to use tariffs and other regulatory measures to reshape U.S. trade relations with other countries, South Korea will have to find a way to manage this risk. For the time being, the approach appears to lean on cooperating with the U.S. while looking for ways to diversify its trade portfolio. The latest emergency government meeting on trade resulted in a decision by the Korean government to keep the existing November agreement with the U.S. in place. Meanwhile, the government and businesses have teamed up to seek new trade and investment opportunities. An example is the recent attempt by both government officials and businesses to promote South Korean shipbuilders’ bid for multiple diesel-powered submarines from the Canadian government. Government officials as well as companies in other sectors of the economy (i.e., automotive) are working together to help the shipbuilding sector secure this bid. The South Korean government is also exploring ways to expand the number of trade agreements with other nations, which also appears to be reflected in increased exports to other regions such as Asia, Europe, and Latin America. However, the sheer size and history of trade with the United States would make it difficult for South Korea to accelerate this realignment in the short term. Hence, without an adequate alternative, the best that Seoul can do is expect continued increased short-term volatility and prepare for a sharp downturn in the economy by maintaining disciplined fiscal and monetary policies.

Conclusion

The recent SCOTUS decision, along with the reaction by the Trump administration, confirms that uncertainty will continue to be the new norm in trade. While there are many unanswered questions about how the U.S. government will deal with the approximately $175 billion in revenue already collected under the IEEPA tariffs over the past year, the recent ruling also casts new doubts on the constitutionality of other tariff measures that the administration has imposed or is thinking about imposing. South Korean trade data indicates that increased uncertainty implies greater volatility in its trade not only with the United States but also with other countries. One way that the government has tried to address this risk is by diversifying South Korea’s trade portfolio; however, it is unclear whether the South Korean economy can be nimble and resilient enough to deal with the fluctuations in the global trade environment brought on by this great uncertainty. The best option for Seoul is to remain engaged with the U.S. administration to address any short-term surprises, exercise maximum discipline in its fiscal policy, and maintain sound monetary and macro-prudential policies to prepare for the worst-case scenario should the need arise for the government to intervene.

Community Adaptation for a Water Festival Without Clean Water